Embedded Finance: Governance and Tech Capabilities

My grandfather opened my first saving account on my 10th birthday(late 80's) and I remember we visited our nearest post office and with all paperwork it took us nearly 2 hours to finally get my account number. Fast forward to future, a few years back when I continued the tradition for my son, I completed whole process in under 20 mins and never left confines of our home in the UK.

Our online and offline worlds are converging at a pace which was never seen before. As the world witnesses explosive growth for internet usage [1], online transactions are breaking all records worldwide [2] . On one side financial transactions are going digital, while, on the other side, banks are closing branches in hoards [3]. People can now walk into stores and walk out with their purchase without ever visiting any POS terminal [4]. Embedded finance is slowly becoming a reality in our digital lives.

As we go through this new wave of financial innovation, it also creates room for newer risks and challenges which need to be governed through well defined policies, processes and technology.

For our society and businesses to truly accept and adapt to these changes, it is imperative that we also build strong foundations of trust which not only allows innovation to flourish but also provides security, reliability, and confidence to the masses, while shielding them from all inherent risks.

Governance which works for all

Financial governance broadly refers to the way companies and entities engaged in financial transactions collect, manage, monitor and control financial information . It includes how institutions track financial transactions, manage performance and control data, compliance, operations, and disclosures.

We have quite a few governance frameworks in use today[5][6][7][8]. A simple cursory read of governance frameworks, such as COBIT[5] or COSO[8] or similar, makes it very clear that to establish an effective governance environment, control concepts and capabilities must be woven into the very fabric of the system. Otherwise, it is nearly impossible to layer new control segments onto a pre-existing enterprise system and to ensure an effective, comprehensive, documentable, maintainable, economical and auditable control environment.

So, where do we go from here?

Broadly, most governance frameworks provides two main inputs to businesses and entities

- Guidance on internal controls required to reduce the risks

- Help to develop, organise and implement strategies around information management and governance

Considering the above frameworks, if we look at embedded finance use cases such as BaaS or BNPL or invoice financing or embedded payments/lending or insurance, these all require strong foundational support from existing financial ecosystems. This foundation not only provides stability, trust and reliability but also flexibility to innovate and drive progression.

We can achieve these through a Universal Governance framework (UGF). All key players ( financial institutions, digital platforms and infrastructure service companies) in embedded finance must work together to build such a system and support the community.

While a lot can be learned and cloned over from existing frameworks. embedded finance (EF) has its own set of peculiar challenges which UGF can look to solve for all participants:

Standardised processes for KYC/AML/CTF and risk management

Each constituency imposes different regulations, rules and requirements for financial transactions but there are some common patterns such as obligations towards Financial Action Task Force (FATF), anti-money laundering (AML) laws and similar. We should consider working towards standardising and digitising the majority of these requirements to make it easier to automate for various EF use cases.

Global user/business identity management

With the latest innovation in Blockchain, Distributed Ledger Technology (DLT) and related new technologies, it has now become easier to maintain and manage “one user/business- one identity” programs. Such provisions and support in a governance framework would be a game changer for the ecosystem.

Standard auditing and reporting templates

Continuous and regular audits are a must to reduce risk and fraud occurrences in any financial system. However, it can also add additional burden and slow down the progression for innovative technologies. These processes can be converted to uniform templates across the ecosystem, which will provide flexibility to EF use case developers.

Processes and regulations for secure data sharing

Security is one of the most important pillars for any governance framework. With the distributed nature of most EF use cases, it is prudent that uniform guidelines are created to share end user and business data across the ecosystems. The framework must consider the ownership aspects of data and define right controls around privacy and consent management.

Focus on ESG

With the climate crises now an inevitable reality, ESG (Environmental, Social and Corporate Governance) should be considered an integral part of any innovative solution. ESG considerations, which range from carbon emissions, human rights, and diversity to customer satisfaction, anti-bribery, and whistleblower protections, should apply to all companies and entities, and UGF can provide uniform guidelines and certification processes.

Many Arab nations have started new programs and initiatives to support innovation in the financial industry[9][10]. These countries are rapidly progressing and adopting the changes needed to usher their citizens into the new era of financial freedom and inclusion. By doing so, they have created an environment to build and nurture an exhaustive and inclusive framework, which fosters the growing need of innovation and enables mass adoption of financial technology.

The Technology Role

It is true that payment is now becoming more of an experience. People using EF do not need to understand how it works and the complexity involved. It is expected to “just work”, due to which technology bears the enormous weight to match expectations. This is a gargantuan task for any digital innovation supporter and decision maker.

Most financial institutions struggle to adapt to new technology or change, unless they are starting from scratch. However, this phenomenon can be made possible for the MENA region where investments have doubled in the last year [13] and UAE government reports suggest the market to grow by 2.5 Billion by the end of 2022 [14] [15]. These signals means there is no shortage of investment or opportunities which are two prime needs for any technological innovation and adoption. The question is how we can utilise this unique moment where a whole ecosystem can be built from scratch.

There are a few things we can do:

- Speak the same language AKA Standardisation

A well known and tested methodology for inter system/network/process to work is to standardise the communication channel. Once all participating components/entities speak the same language (technical standards and specifications) and use the same grammar (API), it is easier to carry out the business. Standardisation can make it a little easy for us to identify, define and build required technological solutions.

Most recently the Kingdom of Saudi Arabia implemented CSF [12] , Open Banking Framework [13] and a multitude of other actions to enable fintech and financial innovation in the region. Neighbouring country Bahrain[10] has also implemented Open Banking regulations. Such initiatives are the first right step towards regulations led enablement of Embedded Finance. However, we must note that Open Banking standards only focus on account and payment data, and it does not include credit, lending, insurance, and other financial products. We believe that technology exists today to easily support such cases and through collaboration, standards could be easily extended to harness the true power of embedded finance.

- Enhancing and Extending the digital infrastructure

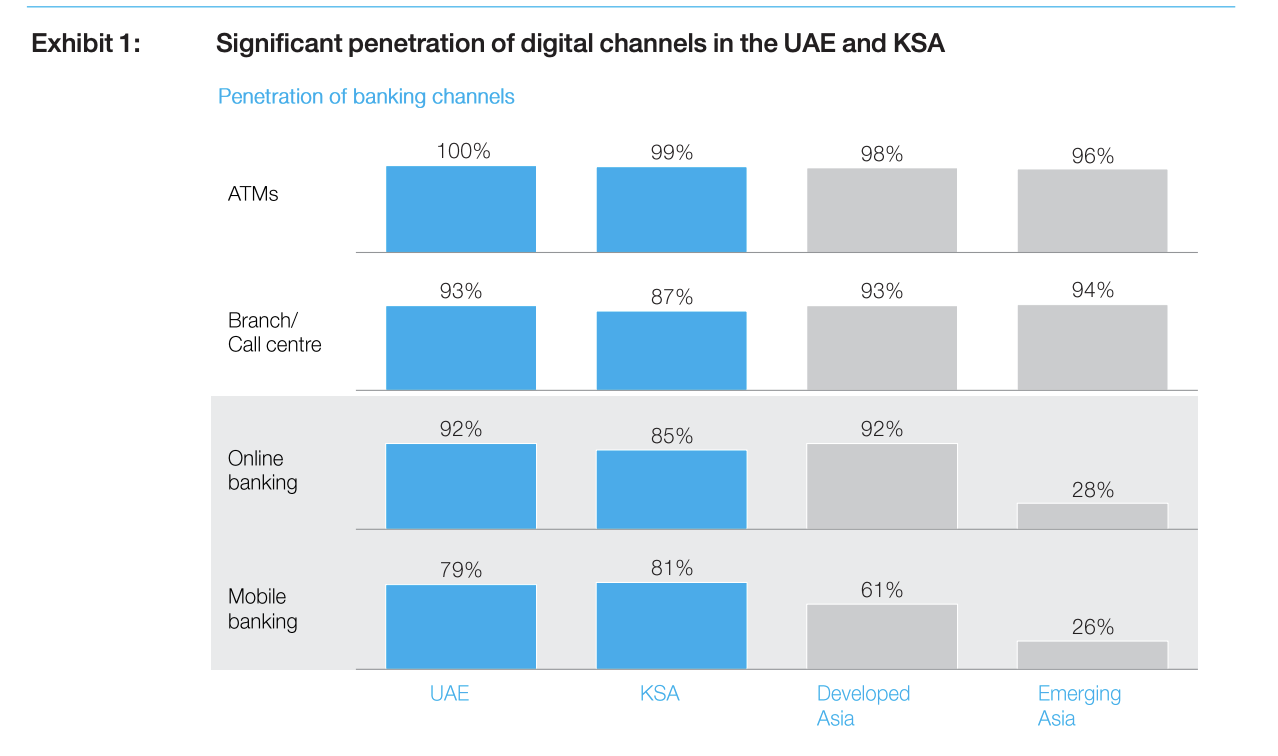

Embedded Finance can be characterised as the stage in the end user journey where the customers of non-financial players are offering financial services. There must exist a transparent process of embedding a financial product at the point of this connection, tailored to the individual user’s needs and often improved by the use of contextual data. For this process to be implemented and executed properly, the digital infrastructure which consists of network, computer storage and transport channels must be improved. GCC nations have the highest percentage of internet users [16] and most banks are already demonstrating digital readiness.

Mckinsey report on digital banking in Gulf (2021)

The next step in the process should be open collaboration between banking and other institutions, which includes technical service providers (TSP) and/or other non-financial institutions. A direct relationship with TSPs and Banking system is the first step towards creating BaaS (banking as a service), which is also the most important case for Embedded Finance ecosystem.

- Automating monitoring, Detection & Compliance

For regulated (Banks, TSPs and Financial institutions) and unregulated (Application providers, small business users) entities to work together, they must cross over the hurdles of compliance, security and fraud detection. Technology can create required bridges through automation. Compliance automation ( compliance as a service) paired with automated fraud monitoring and detection and e-KYC services is picking up in the last few years. The inter-connection of these systems is possible today due to the rise of API (Application Programming Interface) usage across industry[17]. As we create more partnerships and use common standards for authentication and authorisation (such as OAuth and other open ID providers)[18], it is possible to create a shared network, system and database for automated system monitoring and fraud detection. With the guidance of central banks across regions, a single repository of compliant organisations can be created. It is similar to trust services and directory in the UK, which would further help remove barriers of entry for unregulated entities in the embedded finance adoption.

- Design for the future AKA multiverse

Financial transaction and service usage is the norm today but the virtual world is the future. If we were to trust the predictions then this market is on the path to see 20x growth in next 5 years [20]. All this growth would be powered by virtual currencies and a new generation of users/traders.

Virtual currencies are digital representations of value whose transactions occur on online networks or on the internet. UAE has taken the lead in supporting crypto assets [19],paving the way for the development and innovation in this field. Many other countries, hopefully, would soon follow.

Work on connecting these two worlds is making headway. We already have technology to convert virtual currieries to fiat and vice-versa. We can store identities and transactions digitally on a block, sign contracts digitally and audit/track them. Next steps would include connecting physical identities to virtual, linking assets in both worlds, creating value based equivalence (web2 ↔ web3 pipes), and enabling smooth operation and transaction between the two worlds.

Conclusion

In an era where our financial lives are integrated into our digital lives, it is integral to have clear policies and processes to govern this new wave of financial innovation. While embedded finance, like any technological advances, provides opportunities for innovation, we also have to ensure that associated risks are mitigated. Ultimately, the purpose for governance standards and frameworks is to ensure that end-users are able to trust a new technology and benefit from its transformative impact on their lives.

References

[1] https://www.statista.com/statistics/1190263/internet-users-worldwide/

[2] [E-commerce worldwide - statistics & facts - Statistahttps://www.statista.com › ... › Key Figures of E-Commerce](https://www.statista.com/topics/871/online-shopping/#:~:text=As internet access and adoption,4.2 trillion U.S. dollars worldwide.)

[3] https://magazine.northeast.aaa.com/daily/money/savings/why-are-banks-closing-branches/#:~:text=U.S. banks closed a total,1%2C391 branches closed in 2019

[5] COBIT

[6] ISO

[7] NIST

[8] COSO

[9] KSA vision 2030

[10] Bahrain open banking

[11] https://www.bain.com/insights/embedded-finance/

[12] SAMA open banking

[13] https://dealroom.co/blog/fintech-in-the-mena-region-a-rising-star#:~:text=The fintech startup and venture,almost 2x the previous record.

[14] https://www.moec.gov.ae/en/-/fintech-en

[17] https://skaleet.com/en/blog/why-apis-are-essential-for-the-rise-of-embedded-finance/

[18] https://www.oauth.com/oauth2-servers/openid-connect/building-an-authentication-framework/

[19] https://www.mondaq.com/fin-tech/1197116/crypto-assets-regulation-recent-developments-in-the-uae

[20] https://www.brinknews.com/the-metaverse-a-5-year-forecast-of-how-it-will-affect-your-business/

Member discussion